Hey there! First off, if you just got your very first real-deal paycheck—huge congratulations! Seriously, take a second to let that sink in. After all the crazy late-night study sessions, endless assignments, stressful job interviews, or weeks of exhausting skill-building, seeing that hard-earned money landing fresh into your bank account is a massive win. It’s validation. It’s independence. For a couple of hours, you feel absolutely unstoppable, and honestly, you've earned every bit of that feeling.

But then, reality knocks on the door. You open your banking app, look at that new balance, and a weird little wave of anxiety suddenly kicks in. It dawns on you that you're now fully in the driver's seat of your own adult life. Suddenly, things like rent, internet bills, groceries, commuting costs, and subscriptions are all staring you down, waiting for their cut. On top of that, you keep hearing these voices in the background whispering about 'emergency funds,' 'paying off loans,' and 'investing for the future.'

It’s completely normal to feel a bit overwhelmed! Without a clear game plan, it's dangerously easy to watch your money just... vanish. It’s what people call 'lifestyle creep'—where your spending naturally grows to match whatever you're making, leaving you living paycheck to paycheck even when you have a great salary. But don’t worry, you don’t need a complicated accounting degree to protect yourself. All you need is an easy, flexible blueprint to keep you grounded. That’s exactly where the classic 50/30/20 rule comes in.

So, What Exactly is the 50/30/20 Rule?

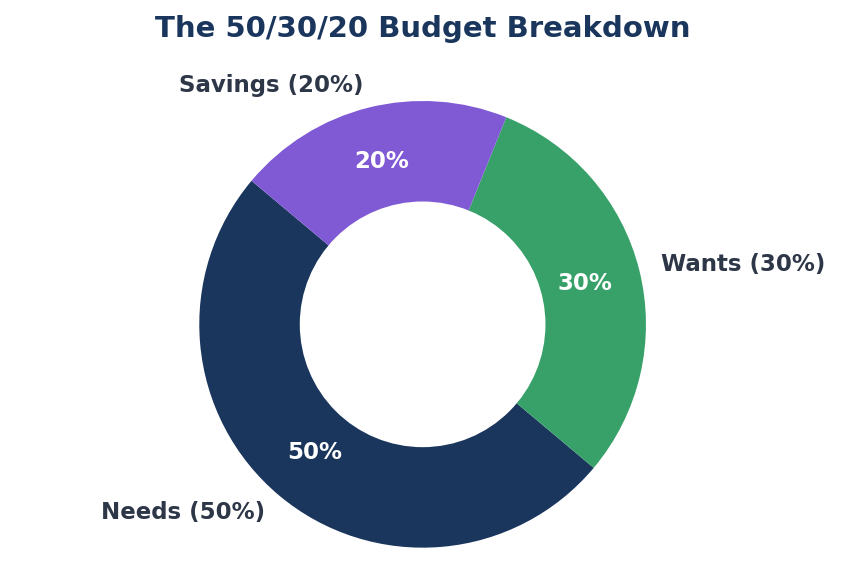

Think of the 50/30/20 rule as an effortless budget filter. Instead of forcing you to meticulously track every single cup of coffee or snack in a massive, painful spreadsheet, this system splits your net take-home pay (the actual cash that hits your account after taxes) into three super simple buckets: Needs, Wants, and Savings.

The formula itself is beautiful in its simplicity: Net Pay = 50% Needs + 30% Wants + 20% Savings/Debt. By looking at your income through these broad lenses, you give every single dollar a real job before you accidentally spend it on impulse buys. It creates a perfect harmony where you easily take care of today's bills, keep enjoying your social life guilt-free, and steadily piece together a massive financial safety net for your future self.

READ MORE ON:The Ultimate Blueprint to Launching Your Online Career 2026

The 50% Bucket: Taking Care of Business (Your Absolute Needs)

Let's start with the heavy hitters: the 50% allocation reserved for your absolute Needs. These are your non-negotiable monthly operational costs. Basically, if you stopped paying for any of these, things would get very bad, very quickly. They keep a roof over your head, food in your fridge, and keep you moving forward professionally.

· Rent and Shelter: Your core monthly rent payment or mortgage, plus any necessary renter’s insurance.

· The Essentials: Electricity, water, gas, and a solid internet or data plan to keep you connected for work.

· Getting Around: Commuter train passes, bus fare, or basic car payments, fuel, and insurance required to get to your job safely.

· Food & Health: Your baseline grocery run (not fancy dinners out) and essential medical insurance or prescriptions.

· Minimum Debts: The absolute minimum payments required on your student loans or credit lines to keep your credit score happy.

Now, if you're starting out in a bustling urban center, keeping all of this under 50% of your paycheck can feel like a tough puzzle to crack. City rent alone loves to try and hijack this whole category! If you run your numbers and find out your needs are eating up 60% or 70% of your cash, don't panic. It's just a friendly sign to optimize. Maybe that means getting a roommate to split the bills, cooking more meals at home, or looking for a more cost-effective phone plan. Small tweaks here go a long way.

The 30% Bucket: Guilt-Free Fun (Your Wants)

Here’s where this budgeting style shines. Most old-school personal finance advice feels like a giant drag because it demands that you cut out all fun, live on ramen noodles, and never buy anything nice. That kind of extreme restriction always backfires—you get tired of it, snap, and go on a giant impulse shopping spree. The 50/30/20 rule completely avoids that nightmare by giving you a clear, guilt-free 30% space just for your Wants.

Wants are the things that make life fun, exciting, and colorful but aren't strictly necessary to survive. We're talking about grabbing dinner out with friends, hitting up concerts, streaming subscriptions, fashion upgrades, weekend road trips, or pursuing cool hobbies. Because you've actively carved out this space ahead of time, you can spend this money with absolute peace of mind. No guilt, no stress, just real enjoyment because your bills are already taken care of.

The trick here is simply being real with yourself about what’s a need and what’s a want. Having home internet is a modern necessity for your job; subscribing to five different streaming channels at once is a lifestyle choice. Going out for a premium coffee is an enjoyable upgrade, not an absolute survival requirement. When times get tight, this 30% bucket is your ultimate safety valve, you can easily dial it back temporarily to keep your whole system stable.

The 20% Bucket: Building Your Personal Financial Fortress

The final 20% of your check is your absolute superpower. This chunk is dedicated completely to your Savings and Future Goals. Think of this as paying your future self first. This is the money that buys your long-term security, gives you career choices, and builds your ultimate independence. Instead of spending it today, you set it aside to outsmart life's surprises and let the magic of compound interest do the heavy lifting.

Golden Rule of Saving: Don't just save whatever happens to be left over at the very end of the month. Instead, automate your savings so that 20% moves out of sight the exact morning your paycheck lands. Live comfortably on the rest!

When you're dealing with your first few paychecks, try tackling your savings in this super smart, three-step order:

1. Build an Emergency Cushion: Stash away three to six months of basic living costs in a separate, accessible account. This is your 'life happens' fund for unexpected doctor visits or car repairs.

2. Crush High-Interest Debt: Once your starter cushion is safe, use this 20% chunk to make extra, aggressive payments against high-interest credit cards or loans to stop interest from draining you.

3. Invest in Your Future: With bad debts out of the way, let that money fly into long-term investments like index funds or retirement plans, giving your money decades to grow quietly.

Putting It Into Action: Your 4-Step Blueprint

Ready to turn this theory into your actual reality? Here is your quick step-by-step game plan for your next payday:

Step 1: Find Your True Net Income. Check your payslip for the actual cash that gets deposited into your bank account—not your gross salary, but the real number left after taxes and insurance deductions.

Step 2: Do the Quick Math. Multiply your net income by 0.50, 0.30, and 0.20. Write those three target numbers down on a sticky note or in your phone—those are your monthly boundaries.

Step 3: Automate the Shield. Set up an automatic transfer in your banking app to instantly push your 20% savings out of your main checking account on payday. If you don't see it, you won't accidentally spend it!

Step 4: Do a Quick Monthly Check-in. At the end of the month, take 10 minutes to review your bank statements. See how close you stuck to your targets. If you went a bit over, don't sweat it! Budgeting is a practice, not a test. Just adjust and realign for next month.

At the end of the day, managing your paycheck isn't about locked handcuffs or making your life small. It's about giving yourself real, lasting freedom and setting up your own world for success. By using the 50/30/20 rule, you take control of your financial story right from page one. Your paycheck is your ultimate tool—use it intentionally, automate your wealth, and enjoy the confidence that comes with true financial independence. You've got this!

READ MORE ON:Lost After Graduation? Use These career persona to Finally Find Your Path

💬 Discussion (0)

No comments yet. Be the first to share your thoughts!

Leave a Response